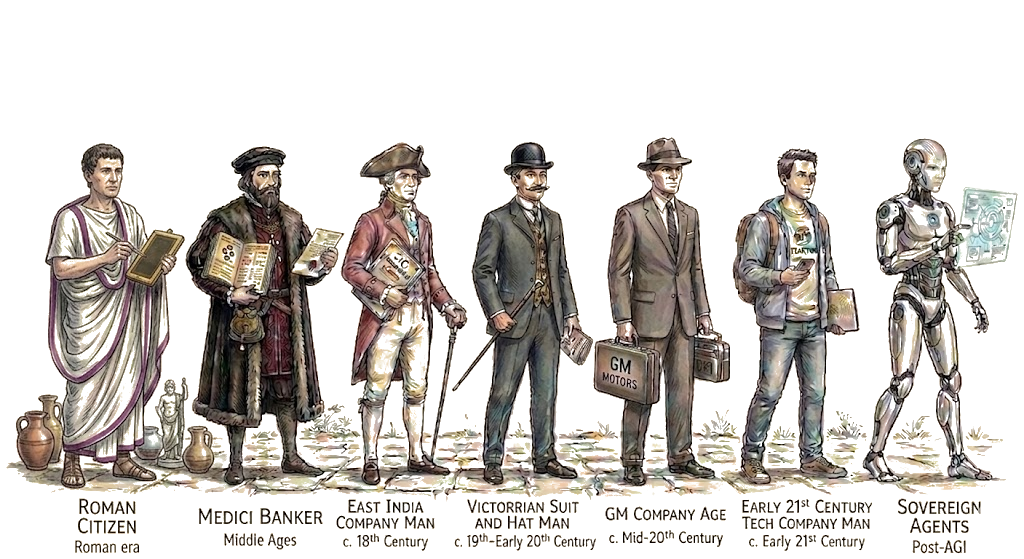

There has been a recent surge of interest in the idea of self-sovereign or “zero-human” companies — entities run by AI agents that can own assets, transact, and grow independently.

The idea is polarizing. Some recoil at the suggestion that AI agents could own property at all. Others dismiss it as impractical. Still others want to push forward as fast as possible without fully thinking through the implications.

But it is worth stepping back. The scope of property rights has never been static. Again and again, law has expanded the range of entities that can hold property, persist through time, and act economically — and almost every such expansion looked dangerous at first, triggering resistance before eventually becoming normalized.

Emergence of Property Rights for Individual Humans

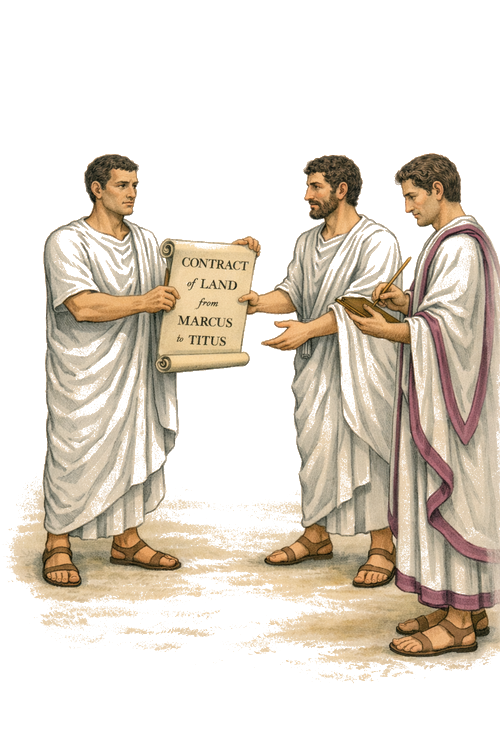

Property rights existed long before Rome. Earlier legal traditions in Mesopotamia had already developed rules around debt, trade, family relations, and civil obligations. Rome’s distinctive contribution was not to invent ownership, but to give it a particularly sharp and durable legal form through the concept of dominium. Roman jurists developed a sophisticated law of ownership, possession, transfer, and inheritance that made private claims more legible, enforceable, and portable across time and distance.

In other words, Roman law became much better at answering questions like: who owns this asset, how can it be transferred, who inherits it, and how can it be defended in a dispute against another private party. But that was different from saying rulers themselves were tightly bound from interfering with property. Roman ownership was a powerful form of law between private parties, not yet a hard constitutional limit on sovereign power. Especially under the Empire, rulers could still interfere with private property through confiscation, taxation, punishment, and political coercion.

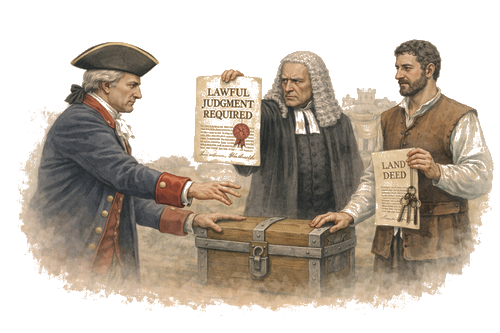

Over the centuries, constitutional developments in England began to add that missing layer by placing progressively stronger limits on arbitrary royal interference with subjects’ liberty and property. Henry I’s Charter of Liberties (1100) objected to abusive exactions and confiscatory practices. Magna Carta (1215) became the most famous milestone in subjecting the ruler to the law of the land, even if much of its later force came through centuries of reissue and reinterpretation. The Petition of Right (1628) sharpened that tradition by rejecting taxation without parliamentary consent, imprisonment without cause shown, forced billeting, and martial law in peacetime. The English Bill of Rights (1689) pushed it further by condemning prerogative levies and declaring grants of fines and forfeitures before conviction illegal.

Taken together, these measures did not make sovereign interference impossible. But they increasingly made it unlawful, contestable, and politically costly. Property was no longer only a matter of legal relations between private parties. It was increasingly becoming something the sovereign could not arbitrarily disturb at will.

That logic later carried into modern constitutionalism. In the United States, for example, the Fifth Amendment (1791) provided that no person could be deprived of life, liberty, or property without due process of law, and that private property could not be taken for public use without just compensation.

The result was a deeper transformation in the meaning of ownership. Property was no longer only about who could hold and transfer assets against other individuals. It increasingly became a claim that public power itself had to justify before overriding. That shift — from ownership as a private legal relation to ownership as something increasingly protected against arbitrary state interference — helped lay the groundwork for the modern individual as an independent economic actor.

Property Rights for Organized Groups

The next major expansion in the history of property rights was the extension of ownership from the individual human to an organized group of humans. This was a profound and highly unconventional step. A group is not a natural person. It has no single body, no fixed lifespan, and no single will. Its members can change, disagree, die, or depart. In that sense, treating a group as a holder of property was a deeply artificial legal move.

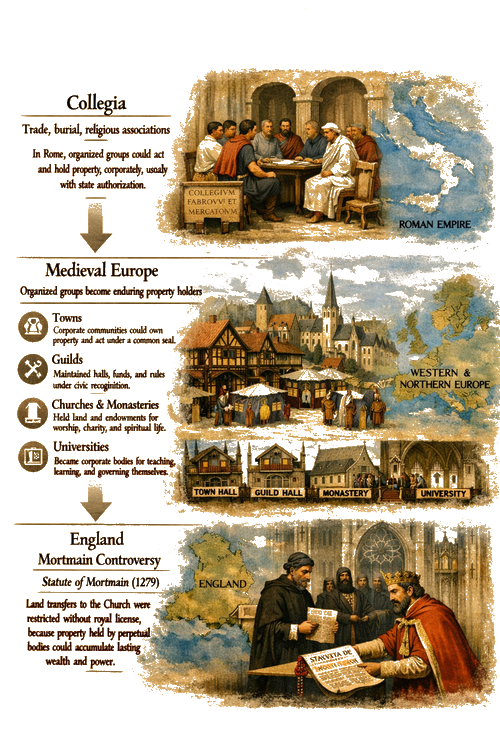

As social and economic life grew more complex, value was no longer created only by isolated individuals or kinship-based households. It was increasingly created and maintained through durable forms of coordination: towns managing common resources, churches holding land and endowments, monasteries preserving wealth across generations, guilds maintaining halls, funds, and shared rules, and universities sustaining teaching and property beyond the lives of their founders and original members. The relevant unit of economic activity had stopped being only the individual and had increasingly become the organized collective.

That created a practical problem for law. If only individuals could own property, then every asset used by a durable collective had to be traced back to particular persons. But that made long-term coordination fragile. Every death, departure, succession dispute, or membership change threatened to unsettle ownership. Shared land, funds, buildings, and rights became harder to preserve when they had to be constantly reattached to changing individuals rather than to the continuing activity itself.

Recognizing the group as a legal holder of property meant treating the organized body, rather than any one member, as the continuing bearer of certain rights and duties in law: it could own assets, receive grants, enter agreements, and in many cases sue or be sued as a unit. It created a stable container for shared assets and obligations. Property could remain with the church even as clergy changed. It could remain with the town even as inhabitants came and went. It could remain with the guild even as masters and apprentices turned over. Ownership was no longer tied only to the lifespan of a single human being. It could now attach to a durable organized body. That made continuity, accumulation, and long-horizon projects far easier. Cathedrals could be built over decades. Universities could preserve endowments. Towns could govern common assets across generations. Organized groups became some of the earliest durable non-human holders of property.

Historical examples of this widening appeared early and then deepened in medieval Europe. In Rome, collegia—including trade, burial, and religious associations—could in many cases act and hold property corporately, though imperial law increasingly required state authorization for their formation. In medieval Europe, that logic became much more entrenched. Towns could become corporate communities capable of owning property and entering agreements under a common seal; the City of London, whose liberties were confirmed by William I’s charter of 1067, is one well-known example of an urban body whose collective legal identity was recognized and reinforced over time rather than created all at once. Guilds maintained halls, funds, and common rules under civic recognition, while churches, monasteries, and universities emerged as enduring institutional bodies capable of preserving land, endowments, teaching, and collective life beyond the lives of their founders.

This expansion was controversial too. Critics worried that once property could be held by perpetual bodies, wealth would be locked away from the ordinary cycle of inheritance and accountability. One famous expression of that fear was mortmain, the “dead hand,” where land held by a church or other enduring body could remain outside the normal turnover of family succession for generations. In England, this concern was serious enough that Edward I’s Statute of Mortmain (1279) restricted transfers of land to the Church without royal license. The concern was not only economic, but political: institutions that could own property indefinitely could also accumulate lasting power.

Still, the boundary had been crossed. Property rights no longer belonged only to individual humans. They could also belong to organized groups that persisted beyond any one member. This was a radical widening of the category of ownership, and it laid the groundwork for the next step: commercial organizations that would not only hold property, but pool capital, pursue profit, and operate at scale.

Pooling Capital Through Shares: The Joint-Stock Company

The next major evolution was not simply that organized groups could own property, but that some were now built to mobilize capital for risky commerce at a scale no household, guild, or monastery was designed to handle.

Towns, churches, guilds, and universities could hold assets across generations, but they were not vehicles for aggregating outside investment into large profit-seeking ventures. That changed with the rise of maritime trade and competitive imperialism. Long-distance oceanic trade required ships, crews, armaments, warehouses, inventories, long planning horizons, and political backing. Capital could be tied up for years, while storms, piracy, war, spoilage, and seizure could wipe out an expedition entirely. These ventures were too large, expensive, and uncertain to be financed comfortably by a single merchant, family firm, or ordinary partnership.

The chartered joint-stock company emerged as the answer. Charter mattered because early oceanic commerce was conducted in a highly adversarial environment: it provided legal standing, privileged access, political backing, and often military protection, making investors more willing to commit capital. Stock issuance made that machine scalable. Shares widened the investor base, spread risk across many participants, made capital more permanent by keeping the enterprise intact beyond a single voyage, and, once transferable, gave investors liquidity.

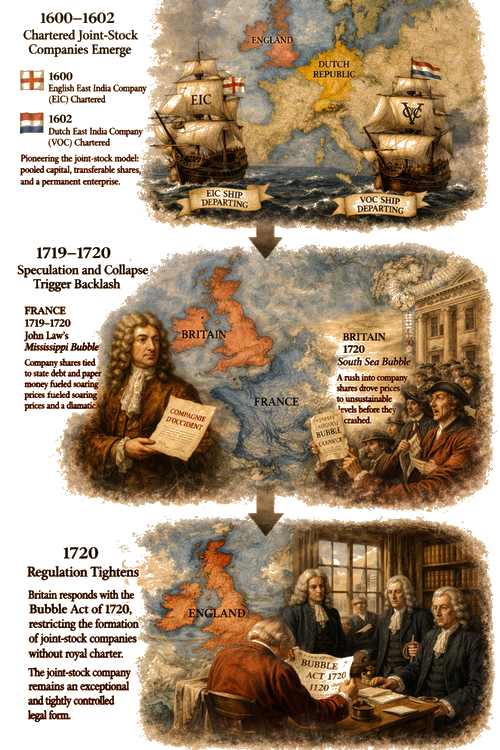

The clearest example was the Dutch East India Company (VOC), chartered in 1602. Here, the older idea of a property-holding collective fused with pooled capital and transferable claims. The company itself owned ships, warehouses, goods, and contracts, while investors held shares in the enterprise—traded in Amsterdam’s stock exchange—rather than direct interests in each voyage’s assets. The English East India Company, chartered in 1600, followed a similar logic, though its move to a permanent joint stock came later.

At this stage, the key innovation was less about shareholder governance than about financial participation: investors were buying into a continuing enterprise and its expected profits, not primarily into day-to-day control.

In effect, the chartered joint-stock company was becoming a machine for aggregating outside resources into a continuing enterprise operating across space and time.

But this expansion quickly generated backlash. In France (1719–1720), John Law built a system in which company shares were tied to state debt and supported by newly issued paper money. Prices rose far beyond what the underlying business could support, and the system collapsed. In Britain, the South Sea Bubble of 1720 followed a similar pattern: investors rushed into company shares, prices soared, and then crashed when expectations outran reality. These episodes made joint-stock companies look reckless and dangerous.

Some quotes from the era that capture the sentiment.

“They cannot commit treason, nor can be outlawed nor excommunicated, for they have no souls.”

— Sir Edward Coke (1552–1634)

“Corporations have neither bodies to be punished, nor souls to be condemned; they therefore do as they like.”

— Lord Chancellor Edward Thurlow (1731–1806)

The response in Britain was the Bubble Act of 1720, which restricted the formation of joint-stock companies without authorization by royal charter. It reinforced the idea that the company remained an exceptional, tightly controlled legal form rather than a generally accessible one. The joint-stock company had proven that capital could be pooled at a previously impossible scale, but scandal and speculation ensured that it remained politically suspect.

That left the next major question unresolved: should the company remain a rare chartered privilege, or become a legal form that ordinary people could access under general law? That struggle would define the next phase of corporate evolution.

From Chartered Privilege to General Incorporation

What changed in the 19th century was the growing idea that incorporation should become a general legal technology rather than a rare favor. The momentum behind this shift came from a combination of commercial pressure and legal reform. Industrializing economies needed more scalable forms of organization for large and durable aggregations of capital, and businesses increasingly resented a system in which access to incorporation depended on political favor rather than predictable rules.

In Britain, the Bubble Act was repealed in 1825, removing one of the major legal restraints associated with the backlash against early joint-stock speculation. At the same time, industrialization—through railways, canals, mining, and later telegraph networks—was creating new pressures for more ordinary and scalable company formation. These were not isolated imperial ventures like the East India companies. They were becoming part of ordinary economic life. That pressure gradually pushed British law toward a new model. The decisive step was the Joint Stock Companies Act of 1844, which allowed companies to incorporate by registration rather than by special charter or private act.

In the United States, the transition was shaped by both constitutional and legislative developments. Dartmouth College v. Woodward (1819) became an important marker because it treated a corporate charter as a contract that states could not simply rewrite at will. It helped weaken the older view that charters were merely revocable political concessions. Over time, American states moved toward broader access through general incorporation statutes, especially for manufacturing and similar enterprises, allowing businesses to form without seeking a special charter each time. In Massachusetts, the stronger step came in 1851, when manufacturing, mechanical, and mining firms could incorporate under general law without needing a special legislative charter.

This was a profound democratization of economic organization. Once incorporation could be obtained under general law, the question was no longer who had enough political access to secure a charter. The question became what rules should govern the companies that ordinary people could now form.

That set up the next major evolution. Once the company form became broadly accessible, the central issue was the allocation of risk inside the firm itself. Who would bear the downside if the company failed? That is where limited liability enters the story.

The Need for Limited Liability

Once incorporation became broadly accessible, the question was no longer who could form a company, but how much risk investors should bear if that company failed.

The old logic of partnership made investors far more exposed. If a firm collapsed, creditors could often pursue the owners personally for unpaid debts. Limited liability changed that rule: shareholders would usually lose only what they had invested, rather than being personally liable for all the company’s obligations.

This was a major shift because it capped downside and made outside investment far more bearable. People of modest means could participate in enterprise without risking total ruin. And as industrialization advanced, that mattered enormously. Railways, mining, steel, and other large-scale enterprises required far larger and more stable pools of capital than older owner-managed firms could easily provide. Limited liability made those capital pools easier to assemble.

This change sparked a serious debate. Critics saw limited liability as an artificial subsidy to the joint-stock form. Skeptics like Adam Smith argued that the owner-managed firm was the purer and more disciplined economic unit: the person with control also bore the full consequences of failure. Once liability was capped, investors could enjoy upside while shifting some downside onto creditors and outsiders. That, critics feared, weakened responsibility and encouraged speculation and recklessness.

Defenders saw the matter differently. Thinkers such as Robert Lowe and John Stuart Mill argued that limited liability expanded economic opportunity. By capping downside, it enabled people without large fortunes to invest, start businesses, and participate in enterprise. Some even saw it as a way of enriching poorer classes and softening class conflict. Mill went further: for very large modern enterprises, the real alternative to the joint-stock system was often not the owner-managed firm at all, but some form of government control. On this view, limited liability was not a distortion but a necessary institutional adaptation to modern scale.

In Britain, the debate produced a series of legal reforms: the Limited Liability Act of 1855, the Joint Stock Companies Act of 1856, and the Companies Act of 1862. Together, they recognized, simplified, and consolidated the limited-liability company as a more ordinary business form.

The doctrine was later hardened by Salomon v. Salomon & Co Ltd (1897). The decision firmly established limited liability for shareholders, the idea that a company can own property, incur debts, and sue or be sued in its own name, and the principle that creditors generally must claim against the company, not its controlling owner personally. Salomon laid the doctrinal foundation for modern corporate personality and strongly reinforced limited liability in the common-law world.

Once ownership could spread across many investors whose downside was capped, the next question was no longer simply who owned the company. It was who actually controlled it.

Separation of Ownership and Control

Once incorporation was broadly accessible and investor downside was capped, ownership could spread far more widely than before. But it also introduced a new problem: ownership and control were increasingly separated.

In earlier owner-managed firms, capital, control, and responsibility were closely aligned: the owner supplied the capital, directed the business, and bore the consequences of failure. As companies grew and shareholding dispersed, that alignment weakened. Ownership remained with shareholders, but control shifted to directors and professional managers. In practice, shareholders often lacked the information, coordination, or incentives needed to direct the firm day to day. The company had become an institution run by managers on behalf of a scattered body of investors. This is the world that Berle and Means diagnosed in The Modern Corporation and Private Property (1932): the separation of ownership and control had become a defining feature of the modern corporation.

This separation made the modern large corporation more workable. It gave firms continuity, because the enterprise no longer depended on the life, attention, or continued ownership of any one person. It gave investors liquidity, because shares could change hands without requiring any transfer of managerial control. And it enabled delegation, because decision-making could be placed in the hands of directors and professional managers chosen for expertise rather than merely for wealth or ownership.

Once ownership and control split, however, a structural question came into view: how were those who controlled the corporation to be constrained? As managerial discretion widened and shareholder oversight became thinner, a new set of issues came into view: how managers could be disciplined, what duties they owed, and in whose interests they were meant to act. Were they agents of shareholders alone, stewards of a larger institution with obligations to workers, creditors, and the public, or fiduciaries of a distinct legal person, the corporation itself?

There was no single statute designed to solve the principal-agent problem created when ownership and control separated. Instead, the United States developed a layered response:

Taken together, these measures did not eliminate the problem, but they created a legal framework through which widely held corporations could be monitored, disciplined, and made more governable.

By this stage, the corporation was easy to form, easy to finance, protected by limited liability, legally distinct from its members, and governed through disclosure and oversight. The next question is whether that form can extend to a non-human system. That is where agentic companies enter the story.